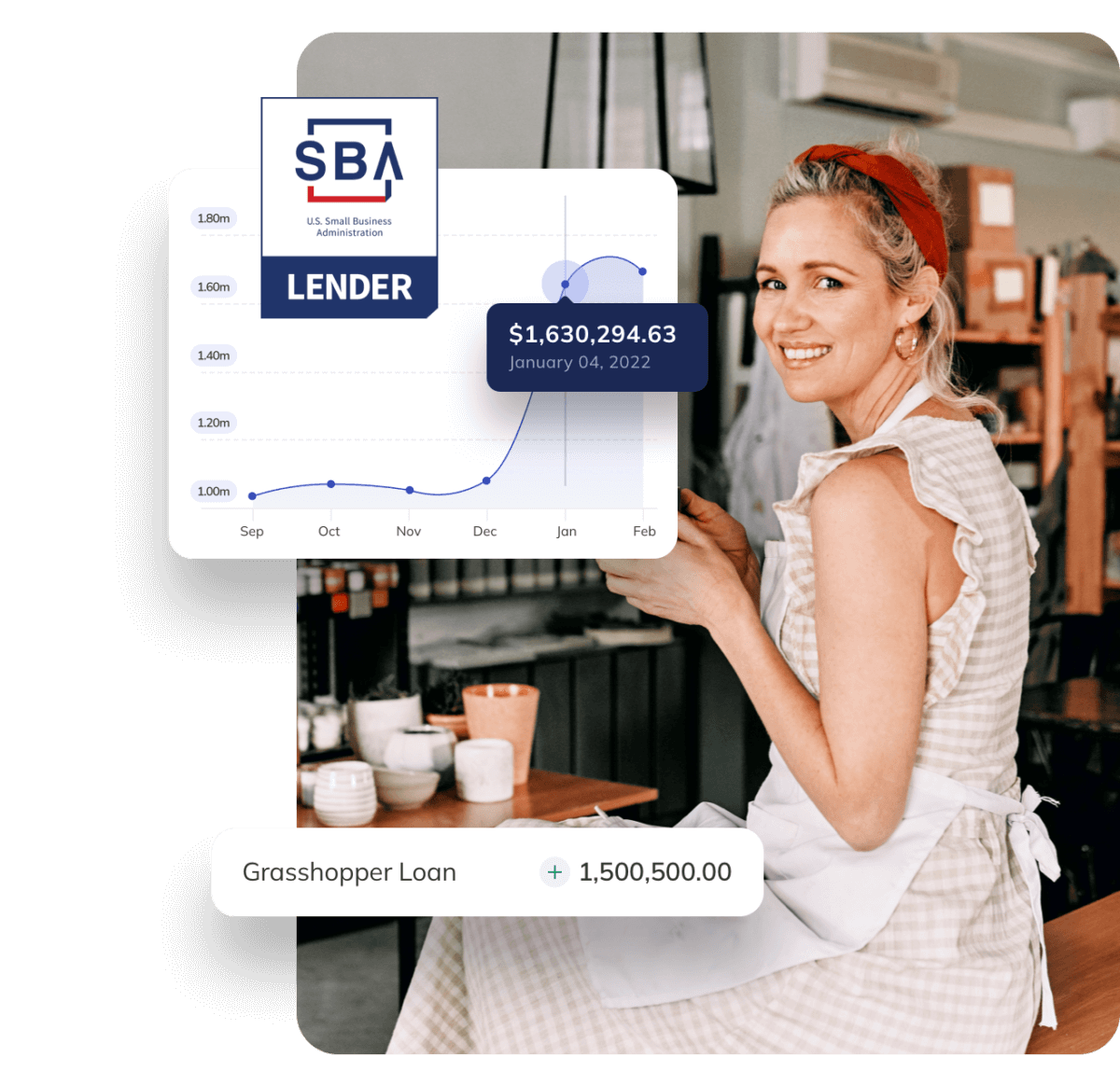

What is an SBA loan?

The Small Business Association (SBA) helps American business owners find funding to help start and grow their companies. With SBA loans, small businesses are able to preserve additional cash for operating purposes since the SBA generally requires less money down on a project. They also offer longer terms and amortizations than conventional lending options, which allows business owners to keep more cash on hand.

The most popular SBA loan program is the SBA 7(a) Loan. The 7(a) program offers financing for virtually all business expenses, making it a good option for acquisitions, partner buyouts, real estate purchases, refinances, and more.

SBA loan vs. traditional small business loan

There are two main differences between an SBA loan and a traditional small business loan: SBA loans typically have longer repayment terms and lower interest rates. Repayment terms with SBA loans can go up to 25 years for real estate and 10 years for other fixed assets and working capital. Traditional loans typically only have terms up to 10 years.

Both types of loans typically are issued by banks, but SBA loans specifically come from banks that participate in the SBA loan guarantee program. This program promises that the SBA will buy back a portion of your loan if you default on your loan or if your business fails. The amount bought back can range from 50%-90% of your loan up to $5 million, depending on the loan program. With a traditional loan, the bank shoulders 100% of the risk if your business defaults, which is why banks often have strict qualifications and require borrowers to have good credit. This is why SBA loans are best for small businesses with little to no credit or may not qualify for a traditional loan.