When cash comes in, businesses want two things at once: immediate access and smart use. Yet keeping money accessible while making it work for you can feel like a juggling act. Interest-bearing business checking accounts strike that balance, keeping cash available to support daily operations while idle funds earn interest quietly in the background.

What Is an Interest-Bearing Business Checking Account?

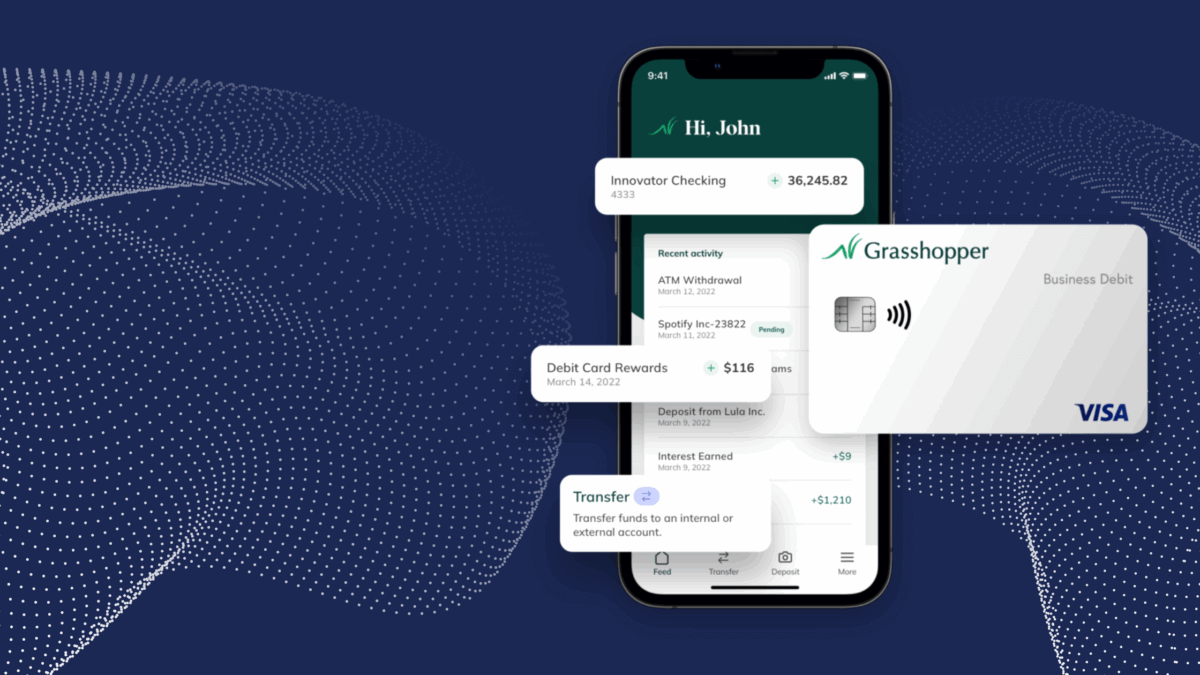

An interest-bearing business checking account functions as a primary operating account while also earning an annual percentage yield (APY) on eligible balances. Funds remain fully accessible for payments, transfers, and withdrawals, but unlike non-interest-bearing accounts, balances generate incremental returns over time.

Most interest-bearing business checking accounts come with eligibility requirements, such as minimum balances or tiered rate structures, which determine how and when interest is applied. Banks typically calculate interest on a daily basis, applying the applicable APY to the portion of the balance that meets account requirements, then credit earnings at regular intervals—often monthly or quarterly—so even modest balances can generate measurable returns when maintained consistently.

Benefits of an Interest-Bearing Business Checking Account

When used strategically, interest-bearing business checking accounts can provide tangible advantages for managing cash, optimizing balances, and supporting day-to-day operations, without forcing trade-offs between access and earnings.

Incremental Returns

Funds used for payroll, rent, or vendor payments can simultaneously earn interest without being moved into a separate account. Interest accrues on qualifying balances over time and is credited at set intervals, creating a steady source of incremental returns. These earnings can help offset routine expenses, support operational needs, or contribute to growth initiatives.

Day-to-Day Flexibility

Unlike traditional savings or money market accounts, interest-bearing business checking accounts are built for frequent transactions. Businesses retain full access to their funds while balances earn interest, allowing you to cover operational expenses without interruption. This combination of liquidity and interest means cash can remain productive even while actively supporting daily operations.

Reduced Fees

Many modern interest-bearing business checking accounts are structured with fewer maintenance fees, helping businesses keep more of what they earn rather than losing money to unnecessary charges. By minimizing costs like monthly service fees, low-balance penalties and per-transaction fees, businesses can reduce administrative complexity and free up resources for essential operations.

Simplified Accounting

With interest accruing directly in the operating account, businesses can reduce the need for frequent transfers between accounts, streamlining bookkeeping and reconciliation. By consolidating operating activity and interest earned in a single set of statements and transaction histories, businesses gain a clear, single source of truth that simplifies reporting, reduces errors, and makes it easier to track cash flow, forecast expenses, and prepare for taxes—all without extra account management.

Operational Efficiency

Because the account combines liquidity and interest-earning capacity, businesses can reduce the number of accounts they manage and focus on the ones that actively support operations. This not only simplifies oversight, but also reduces the risk of inactive or dormant accounts, which can tie up cash, create extra administrative work, and increase the chance of overlooked fees.

Access to Digital Tools

Some interest-bearing checking accounts go beyond the basics, offering features and functionality that make financial management faster and smarter, such as automated workflows for bill pay, advanced debit card controls, real-time transaction monitoring, and direct integrations with accounting, invoicing or payment platforms. Certain accounts even allow multi-user access with dual approvals and customizable permissions, giving businesses greater control and new capabilities they might not find with a standard checking account.