Income Statement

An income statement, also called a profit & loss (P&L) statement, is the most common and critical financial statement. All your income and expenses over a given time are summarized on an income statement to show your company’s financial performance. By looking at an income statement, you can determine if a business is generating a profit or spending more than it earns. This statement is often shared as a quarterly and annual report to show financial trends over time.

Information on an income statement includes:

- Revenue: the amount of money coming in

- Expenses: the amount of money being spent

- Costs of Goods Sold (COGS): the cost of all the parts it takes to produce what the business sells

- Gross Profit: total revenue minus COGS

- Operating Income: gross profit minus operating expenses

- Income Before Taxes: operating income minus non-operating expenses

- Net Income: income before taxes minus taxes

- Earnings per share (EPS): net income divided by the total number of outstanding shares

- Depreciation: the extent to which assets have lost value over time

- EBITDA: earnings before interest, taxes, depreciation, and amortization

There are two commonly used methods for reading an income statement. Using both of these methods will allow you to accumulate the most insights into your business.

Method 1: Vertical Analysis

Vertical analysis is when each line item is listed as a percentage of gross sales rather than exact amounts of money. This analysis makes it easier for financial statements to be compared across periods and industries because you can see relative proportions. This method of analysis also helps with determining whether or not performance metrics are improving.

Method 2: Horizontal Analysis

Rather than looking at each line item as a percentage, horizontal analysis reviews and compares changes in the dollar amounts in a company’s financial statements over multiple reporting periods. Using horizontal analysis makes financial data consistent per the generally accepted accounting principles (GAAP), hence making it important for investors and analysts.

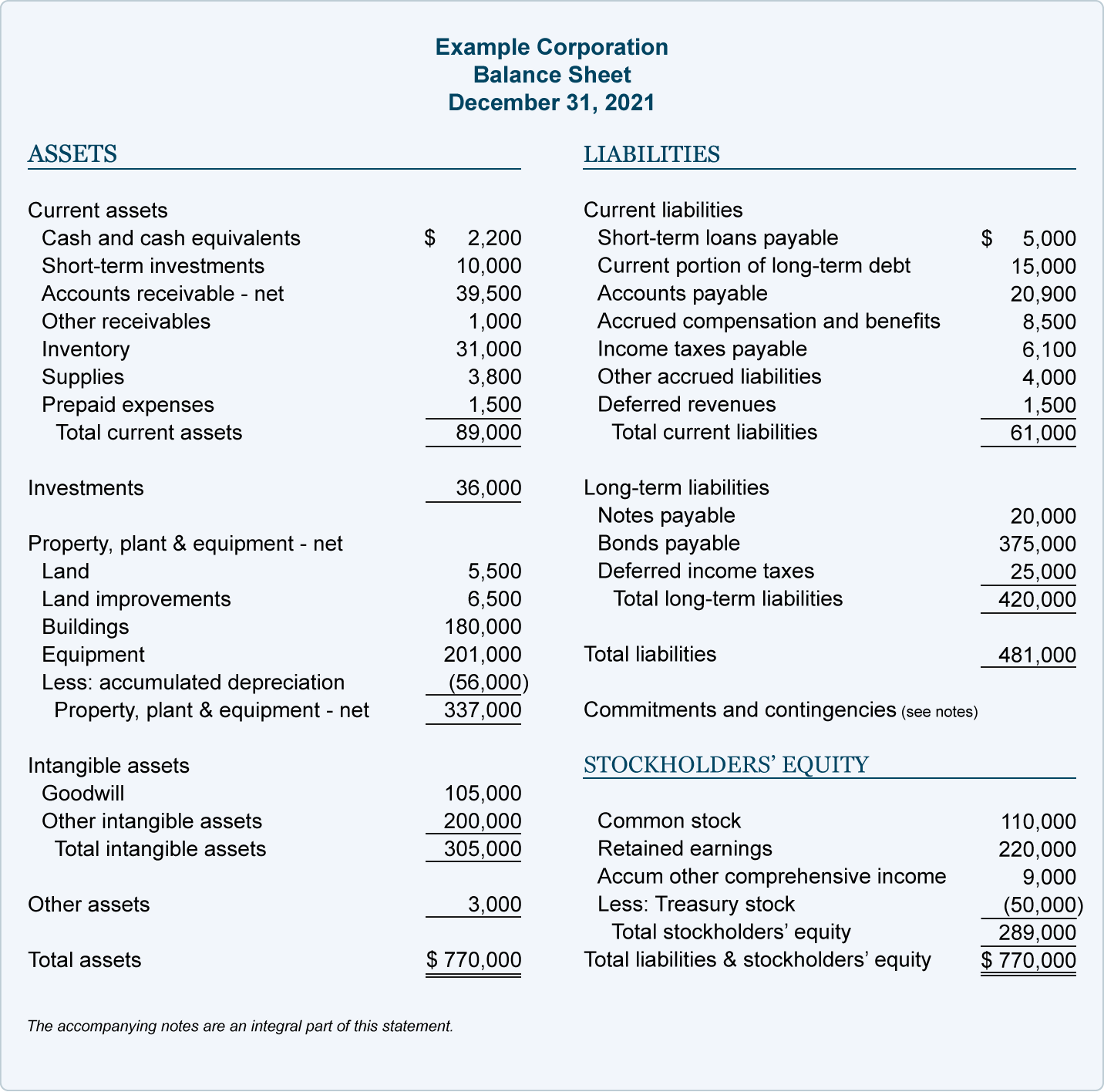

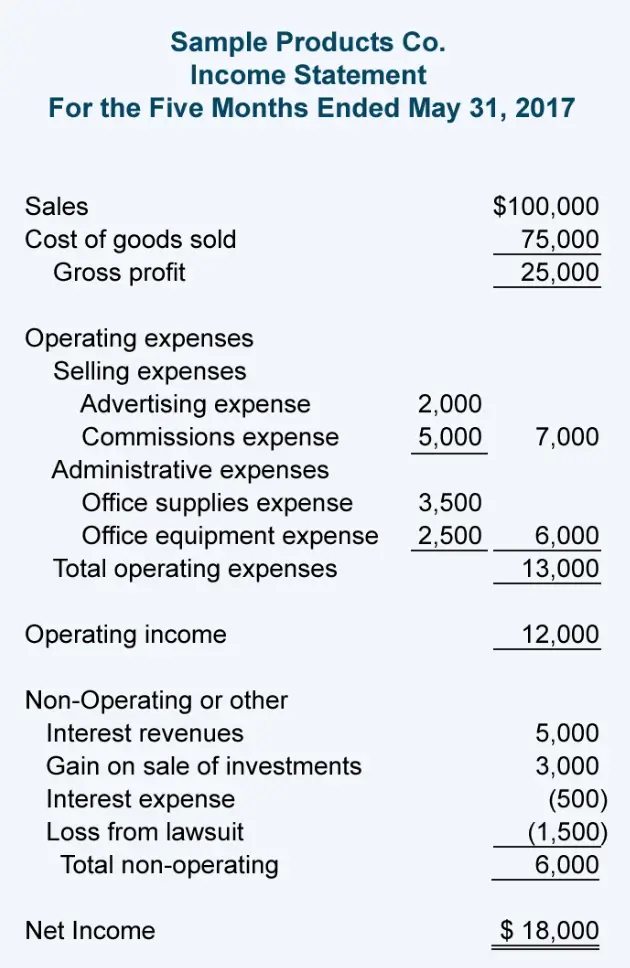

This sample Income Statement from Freshbooks shows the line items reported, the layout of the document and how it differs from an income statement: