Many business owners build their operations from the ground up, learning financial management along the way. In the early stages, using a personal card for a quick vendor payment or accepting client revenue into a personal checking simply feels more efficient. While this is a common starting point, what begins as a temporary convenience can quietly turn into expensive complications later.

Separating your business and personal finances isn’t just good practice. It’s a vital layer of protection, and one of the smartest decisions you can make as a business owner. Here’s why.

Commingling: The Financial Liability You Might Not Know You Have

Commingling is the technical term for mixing personal and business finances. It may sound like an unfamiliar concept, but chances are you’ve already done it more than once without even realizing it. Paying a software subscription with your personal card, covering a business lunch from your personal checking, or depositing a client payment into your personal account are all common examples. Any time business and personal finances intersect without clear separation, it constitutes commingling.

The problem isn’t when it happens once. It’s when it becomes a habit.

Entrepreneurs often plan to open a separate business account once they hit a certain revenue milestone or when operations feel more “established”. But until that moment arrives, allowing the financial overlap to continue makes untangling it later far more time-consuming and expensive than establishing a clear separation from day one.

The good news: opening a dedicated operating account for your business is no longer a lengthy administrative process. Digital banks like Grasshopper enable you to open a business checking account online in a little as 5 minutes, making it easy to establish a clear financial boundary for your business without jumping through hoops.

The Corporate Veil: How Your Business Entity Protects You and How Commingling Puts It at Risk

When you establish a formal business entity, you create what legal and financial professionals call a “corporate shield,” the legal separation between you as an individual and your business. This separation is what insulates you from potential liabilities, debts and legal obligations your business may face.

In the event that your business can’t pay its debts or gets sued, your personal assets (including your home, car, and savings) are legally protected. The business stands alone as the responsible party, assuming its financial obligations on its own merits rather than exposing you personally. However, this “shield” is not unconditional. It must actively be maintained, and mixing your personal and business finances is one of the fastest ways to compromise it.

In legal disputes, commingled finances are one of the biggest red flags a court looks for. It introduces the risk of a legal doctrine known as “piercing the corporate veil.” This means that if a court decides you and your business have been operating as a single entity rather than keeping distinct boundaries, your legal separation can be dissolved. At that point, creditors or plaintiffs are no longer limited to pursuing your business assets; they can target your personal holdings to satisfy claims.

Ultimately, the most straightforward way to prevent your corporate protection from being challenged is to maintain absolute separation with a dedicated business account. One clear boundary for the entity, and one for you personally.

Tax Implications: What the IRS Sees When Finances Are Mixed

Tax season is already stressful. But believe it or not, when personal and business finances are mixed, it gets more complicated. Commingled accounts are highly scrutinized by the IRS, because a lack of separation can signal underreported income or unsubstantiated business deductions that don’t quite add up.

To regulatory auditors, a bank account where business revenue and personal deposits flow together presents a significant compliance risk. Even if an audit clears your business of wrongdoing, the process itself demands substantial time, money, and stress, all of which can be avoided.

Not only that, but mixing finances can lead to paying more taxes than necessary by creating what accountants call the “missing deduction” problem. When legitimate business expenses are buried inside months of personal grocery runs, rent payments, and streaming subscriptions, legitimate deductions are easily overlooked. This results in artificially inflated tax liability, simply because the supporting documentation lacked the necessary organization to substantiate the claim.

And on top of that, if you work with a certified professional accountant (CPA) or bookkeeper, mixed finances mean more hours spent untangling transactions, which translates into a higher bill at the end of tax season. Every hour your accountant spends manually untangling personal transactions from business expenses results in higher professional fees at the end of the year.

Establishing a dedicated business account streamlines the entire accounting workflow. With every transaction in one place, tax prep is straightforward and your deductions are easy to defend. Best of all, with a Grasshopper business account, you can integrate directly with accounting software like QuickBooks, Autobooks, Freshbooks and Xero (beta), turning manual bookkeeping into a simple, one-click export at the end of the year.

Growth Blindspot: How Commingling Distorts Business Profitability

One of the most important questions business owners ask themselves is: Is my business actually profitable? Not just revenue coming in, but real net income after expenses. When personal and business finances are mixed, that question becomes hard to answer.

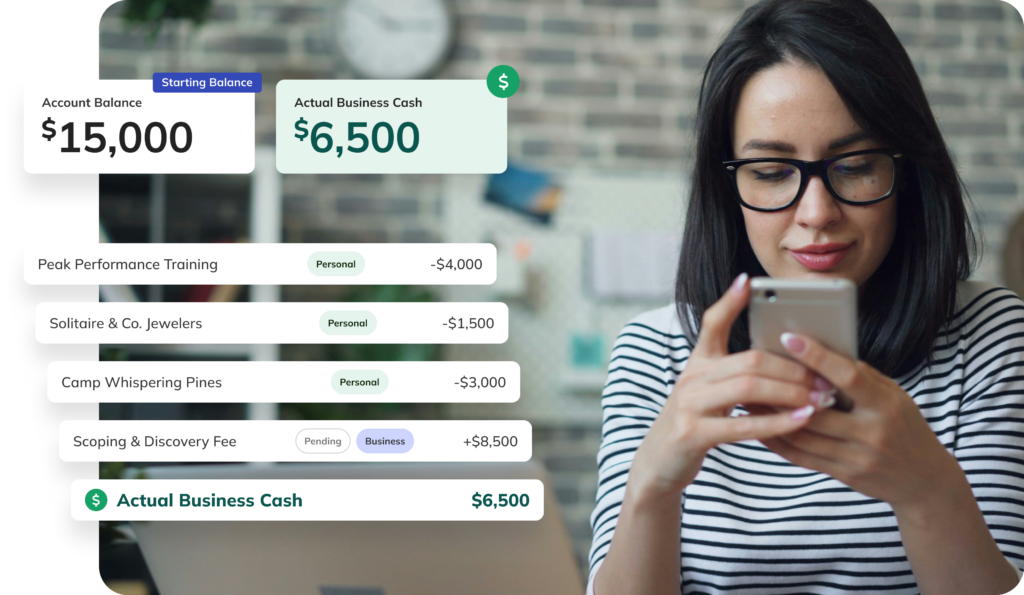

The Balance Sheet Illusion

If your account shows $15,000 at the end of the month, but $4,000 went to a personal trainer, $1,500 went toward purchasing a friend a gift at a local jeweler, a $3,000 expense for your kids’ summer camp, and a $8,500 client payment hasn’t cleared yet, your actual business position looks very different from what the balance says. Without clear separation, that kind of mental math becomes a constant exercise, and there’s no guarantee it won’t go wrong at some point.

When personal and business finances mix, your business figures no longer reflect reality, making it nearly impossible to track your true profitability or make smart growth decisions.

The Impact on Your Business Credit

Many business owners don’t realize that their business can build its own credit score, separate from their personal one. But that process starts with a dedicated business bank account. Without one, every loan application, every vendor relationship, and every future financing opportunity gets tied back to your personal credit history instead of your business’s track record.

A dedicated business bank account gives you an accurate picture of what’s coming in, what’s going out, and what your business is actually worth.

Compliant Compensation: The Right Way to Pay Yourself

Once there’s a clear, accurate picture of what your business is earning, the next immediate question most owners ask is: then, how do I actually pay myself? The answer depends on your business structure, and getting it right is a clear expression of financial separation in practice.

- Owner’s Draw (LLC / Sole Proprietor / Partnership): A direct transfer from the business account to your personal account, recorded as an equity distribution rather than a business expense. It does not appear on a W-2, but must follow a consistent schedule and be categorized correctly in the books to maintain a clean distinction between operational cash flow and personal compensation.

- Reasonable Salary (S-Corp / Corporation): A fixed, documented amount processed through payroll and subject to standard employment taxes. The IRS requires that owner-employees in these structures receive compensation comparable to what the business would pay an unrelated employee for the same role. Drawing money informally on top of a documented salary, without proper payroll processing, is one of the patterns most likely to trigger regulatory scrutiny.

Regardless of structure, the principle is the same: your personal compensation should follow a consistent, documented process, a fixed amount, transferred on a regular schedule, clearly recorded in your books. The moment you start pulling from the business bank account as needs arise, the boundary between business income and personal spending begins to blur, and with it, the integrity of your financial records.

Building a Clean Workflow: Habits That Keep Your Business Protected

By this point, the value of separating personal and business finances should be clear. But understanding the necessity and actually building the habit are two different things. Here’s how to set up a financial workflow that keeps your records pristine, all while managing your money with the discipline of an established enterprise.

- Open a Dedicated Business Bank Account. Before you can organize your cash flow, you need a clean place to put it. If you are still running your company out of a personal checking account, stop immediately. Opening a separate, dedicated business bank account establishes the legal and financial boundary your business needs and gives you a clean slate to build your financial workflow.

- Stop Using Your Personal Account for Business Expenses. If you have been treating your business account like a personal piggy bank or vice versa, it is time to draw a hard line in the sand. Commit to never swiping your corporate card for personal meals, family shopping sprees, or lifestyle bills and only using your business bank account for company expenses. Drawing a clear boundary from day one is the single most important step to keeping your finances compliant and your records clean.

- Assign Yourself a Salary. The same way you would pay one of your employees, set a fixed amount, transfer it to your personal account on a regular schedule, and treat it as your personal income from that point forward. Many business owners skip this step and simply draw from the business account as expenses arise, which makes it nearly impossible to distinguish legitimate business expenses from personal spending. A consistent salary structure keeps both accounts clean and your records accurate.

- Use a Dedicated Business Debit Card. Commit to using it for every professional purchase, regardless of the amount. A client lunch, a domain renewal, a monthly software subscription. If it’s a business expense, it belongs on the business card, without exception.

- Consult a CPA Early. Don’t wait until tax season or an audit to bring in an expert. Partnering with a professional accountant early on ensures your business structure is set up properly from day one, helps you establish clean bookkeeping boundaries, and gives you a definitive blueprint for what is—and isn’t—a legitimate business write-off. Catching bad habits before they become deep-rooted routines will save you thousands in forensic accounting fees later.

- Establish a Monthly Reconciliation Routine. Clean habits require regular maintenance. Block out 30 minutes at the end of every month to review your bank statements, categorize your transactions, and match receipts. When you audit your own books monthly rather than once a year, you catch accidental personal swipes immediately, keep your dashboard accurate, and ensure your finances stay completely organized without the stress of a year-end crunch.

- Automate with an AI-Powered Review. Keeping your finances clean doesn’t have to mean spending hours over spreadsheets. By leveraging a financial platform with secure, MCP-based AI connections, your monthly review can happen instantly, giving you enterprise-grade accuracy with zero manual effort.

This is where Grasshopper makes a real difference. By pairing these foundational habits with a business bank account built for modern workflows, a tedious financial checklist transforms into a system that runs on autopilot, delivering the crystal-clear separation, visibility, and efficiency your business needs to stay protected and scale.

Grasshopper: The Complete Toolkit to Keep Your Business Finances in Order