Creating a budget is rarely a business owner’s favorite aspect of running their business, as it can take a lot of time and energy. However, it’s a must-have for every small business that wants to stay financially healthy and become as successful as possible. A business budget works as a financial road map, offering you a detailed plan of where you’ll spend your money monthly or annually.

Why do you need a budget?

There are many benefits to creating a budget for your small business. A well-constructed budget can help you with the following:

- Forecasting the money you’re expected to earn

- Planning where to spend your money

- Identifying what expenses need to be cut

- Pointing out any leftover funds that can be reinvested

- Predicting slow months

- Keeping you out of debt

Overall, budgeting makes it easier to run your business by ensuring you’re spending money in the right places. So, creating a budget is an excellent place to start if you want to run your business efficiently.

How to create a budget

Creating a budget can be boiled down to three main steps:

Step 1: Estimate your revenue

Before you can figure out where to spend your money, you have to know how much money you have to use. Spending more money than you bring in often leads to borrowing money, which defeats the purpose of having a budget in the first place. To create a realistic revenue estimate for the upcoming year, use previous years’ revenue figures as a reference point, taking into account all income sources.

Step 2: Analyze your costs

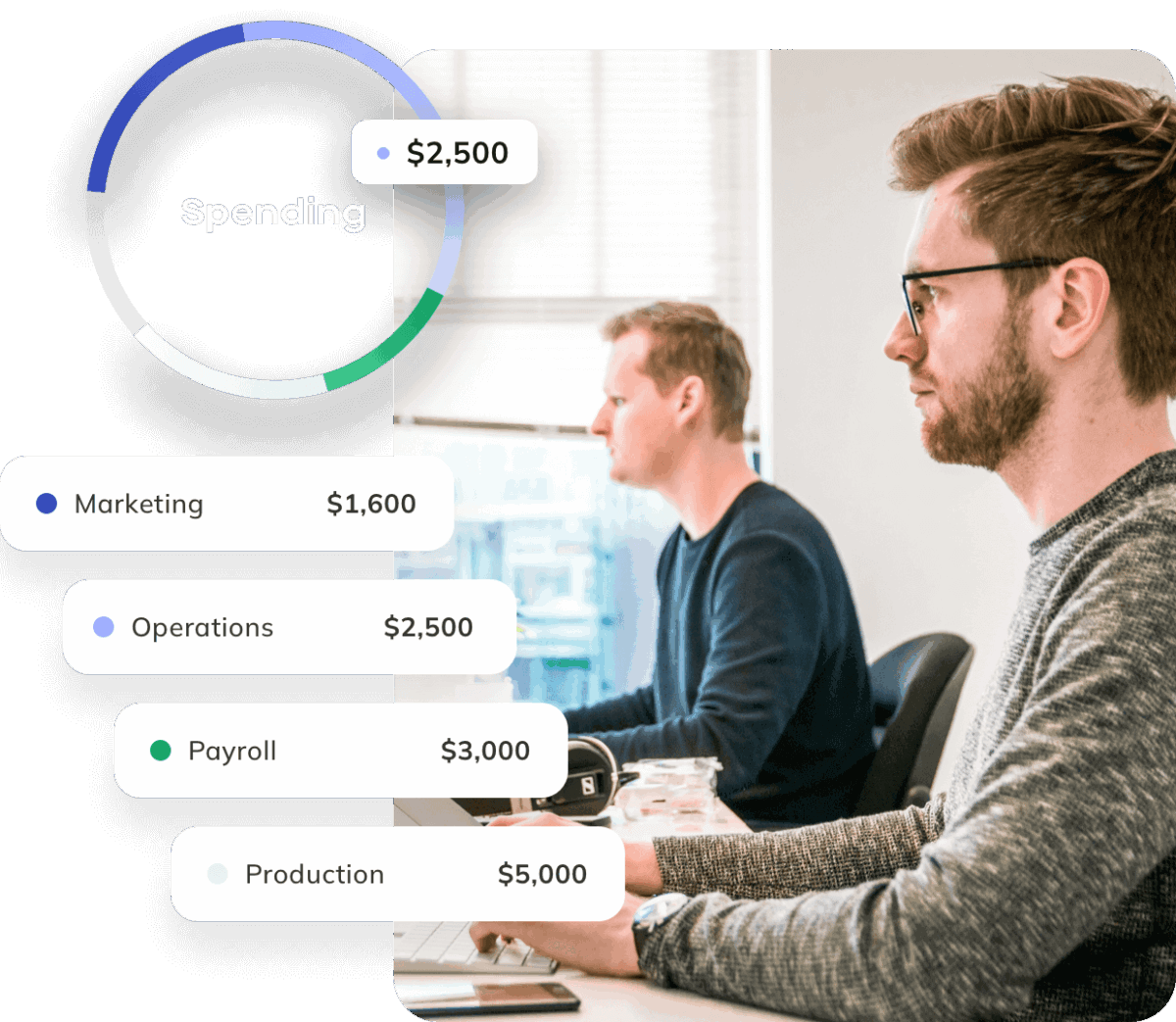

There are three types of costs that you need to take into account:

- Fixed costs: these are the costs that stay the same month to month, such as rent, internet, payroll, etc. These costs should be the easiest to calculate since they remain constant.

- Variable costs: these costs differ from month to month. Examples include electricity, travel, or marketing costs. To better predict how these variable costs fluctuate over time, add the total costs at the end of each month. After a while, you can accurately estimate how much of your income will need to be allocated for these costs.

- One-off costs: these costs are not paid for monthly and are often unexpected, such as replacing broken equipment. You want to ensure that part of your budget includes an emergency fund for these expenses.

Pro tip: some costs can be negotiated. For businesses that rely on suppliers, it may be possible to negotiate discounted rates on the products or services you need, so don’t forget to have these conversations with your suppliers as you calculate your annual budget.

Step 3: Put it all together

Once all the information is collected, it’s time to piece everything together. After subtracting your fixed and variable costs from your total revenue and determining how much to set aside for possible one-off costs, you will know how much you’re truly profiting.

Creating a profit & loss statement (also referred to as an income statement) is a great way to see all your revenue and expenses in one place, thus making it easier for you to know where you can focus your finances.