Navigating SBA programs can feel complex, especially when you’re trying to determine which one truly fits your business needs. The U.S. Small Business Administration (SBA) offers several programs to help small businesses grow, most notably, the SBA 8(a) Business Development Program and the SBA 7(a) Loan Program.

While both support small businesses, they do so in very different ways. Understanding how they compare, and how a Preferred Lenders like Grasshopper simplify the process, can help you make the right financing decision.

SBA 8(a) Program: Pathway to Federal Contracting

What Is the SBA 8(a) Program?

The SBA 8(a) Business Development Program is a certification and development initiative for small businesses owned by socially and economically disadvantaged individuals. It’s not a loan; it’s a gateway to exclusive federal contracting opportunities and hands-on mentorship from industry leaders.

For small businesses, breaking into federal contracting can be a game-changer. The U.S. government is the world’s largest buyer of goods and services, awarding hundreds of billions of dollars in contracts each year, and a significant portion is set aside specifically for small and disadvantaged businesses. These opportunities provide more than just revenue; they offer stability, long-term partnerships, and a pathway to scale. By earning an 8(a) certification, small businesses can position themselves to compete for—and win—contracts that drive sustainable growth and establish credibility in new markets.

Key Benefits of SBA 8(a) Certification:

- Access to federal contracts reserved for SBA 8(a) participants

- One-on-one mentorship and business development resources

- Networking with federal agencies and prime contractors

- Nine-year program duration: four years developmental + five years transitional

The Path to SBA 8(a) Certification

While the benefits of SBA 8(a) certification are significant, achieving them requires meeting high standards. The SBA 8(a) certification process is rigorous, requiring applicants to demonstrate ownership, financial eligibility, and operational readiness through detailed documentation. The SBA’s review ensures that only capable, compliant, and resilient businesses are approved, making certification both a challenge and a powerful credential that signals excellence and readiness to compete at the federal level.

SBA 8(a) Program Eligibility: Who Can Apply?

The SBA 8(a) Program is intended for small businesses owned by individuals who have faced social or economic disadvantages, which means not every small business will qualify. But for those that do, the benefits can be transformative. To ensure the program benefits those it was created to help, the SBA sets specific eligibility requirements that an applicant must meet:

- 51% ownership and control by U.S. citizens who are socially and economically disadvantaged

- Small business status under SBA size standards, which are based on industry-specific limits for average annual revenue or number of employees.

- Personal net worth below $850,000, excluding home and business equity

- Adjusted gross income below $400,000 and assets under $6.5 million

- Demonstrated good character and potential for success

Socially disadvantaged groups recognized by the SBA include Black Americans, Hispanic Americans, Native Americans, Asian Pacific Americans, and Subcontinent Asian Americans. Others may qualify by proving disadvantage on a case-by-case basis.

SBA 7(a) Loan Program: Flexible Funding for Growth

What Is the SBA 7(a) Loan?

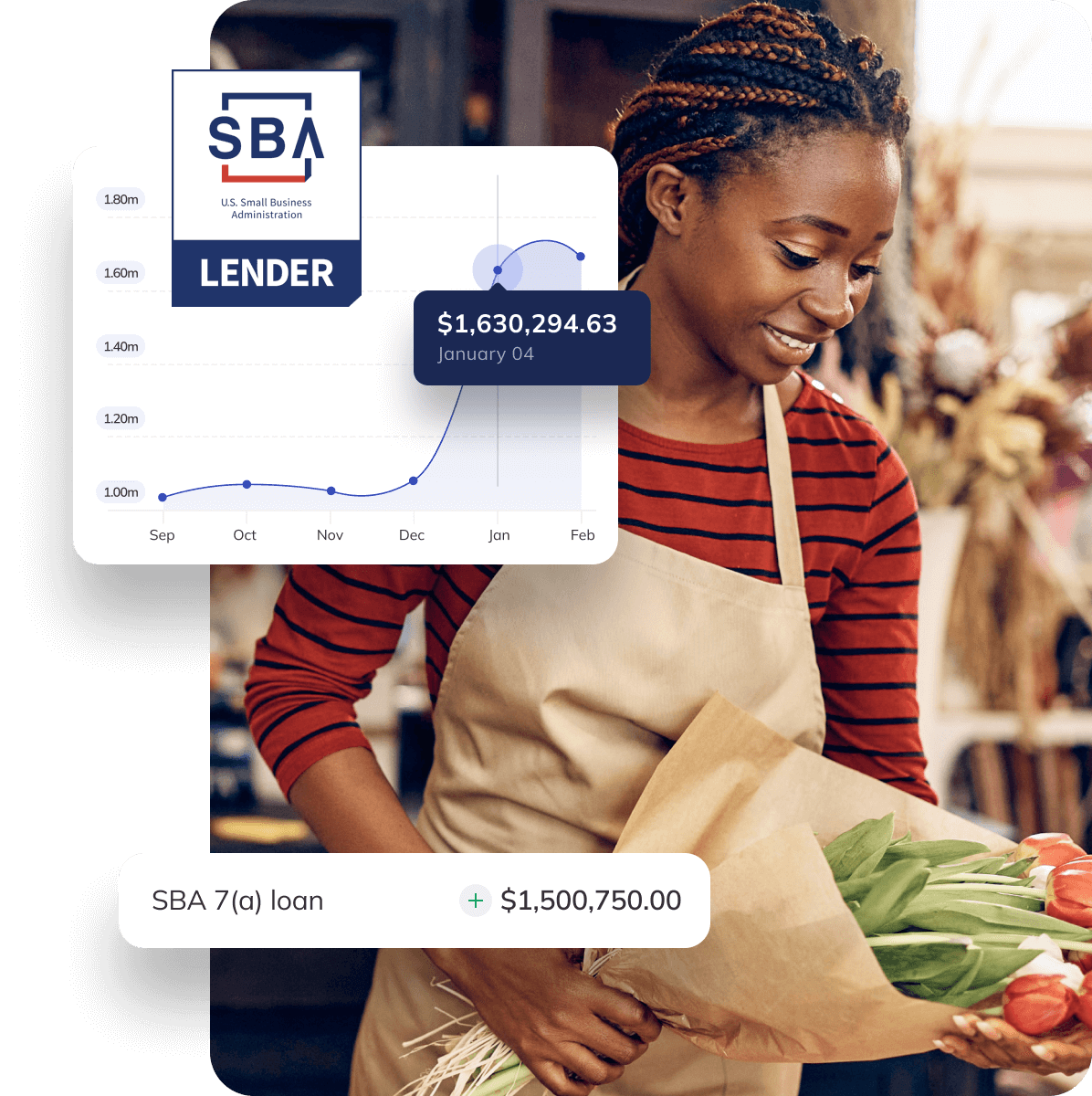

The SBA 7(a) Loan Program is the SBA’s flagship financing solution designed for small businesses that need capital to start, expand, or strengthen operations. It’s one of the most versatile options available, offering funding for nearly any business purpose and making it easier for borrowers to qualify thanks to an SBA guarantee.

Because the SBA guarantees a portion of each loan, lenders take on less risk, which helps more small businesses secure financing with flexible terms and lower down payments. This guarantee means that the government promises to cover a portion of the loan if the business can not, making it easier for lenders to offer more favorable terms to borrowers.

How It Works:

- Small businesses can borrow up to $350,000 through the SBA 7(a) Small Loan Program, while the standard SBA 7(a) Loan Program offers financing up to $5 million.

- Offers competitive interest rates governed by SBA guidelines, ensuring they remain within allowable limits, and are often lower than traditional term loans.

- Down payments can be as low as 5%, with higher requirements for certain acquisitions or startups.

- Repayment terms are flexible, allowing up to 25 years for commercial real estate and up to 10 years for working capital, equipment, and business acquisitions.

- Funds can be used for nearly any business purpose, including working capital, equipment or real estate purchase, expansion, debt refinance, or business acquisition.

- There is no prepayment penalty for terms under 15 years, giving borrowers added flexibility.

- The SBA guarantees up to 85% for loans under $150,000 and up to 75% for loans above that threshold, increasing access to capital and making financing more attainable for small businesses.

Understanding SBA 7(a) Interest Rates

Before exploring eligibility, loan amounts, and terms, it’s important to understand how interest rates work within the SBA 7(a) program. The SBA sets maximum allowable rates that lenders can charge, and these caps vary depending on the size of the loan. While many lenders price below these ceilings based on a borrower’s credit profile, the SBA limits give small business owners and founders a transparent sense of what the cost of capital may look like. Below is a breakdown of the current maximum variable interest rates permitted under the program.