Before diving into timing, limits, or availability, it’s important to start with a clear definition of what a mobile check deposit actually is and how it compares to a traditional check deposit.

What Is a Mobile Check Deposit?

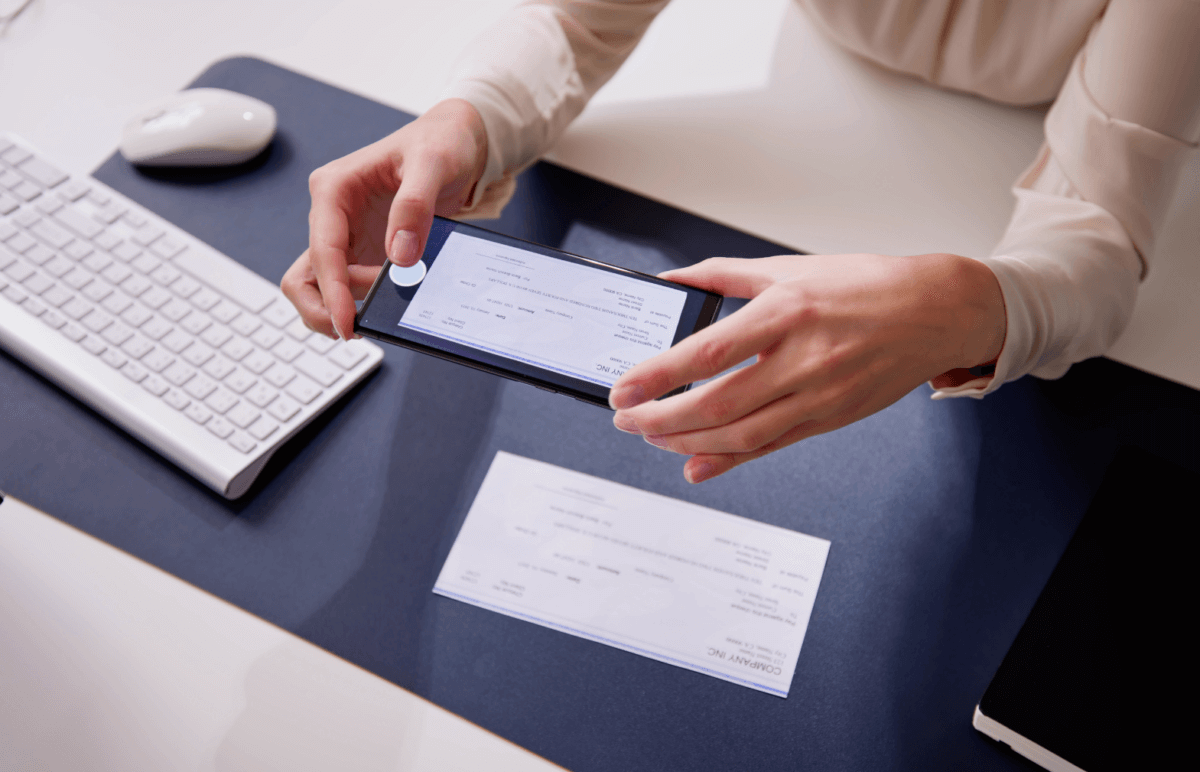

A mobile check deposit allows you to deposit a paper check using your bank’s mobile app by submitting photos of the front and back of the check. This process is commonly referred to as remote deposit capture (RDC).

Although the submission happens digitally, the check is processed through the same traditional banking system as an in-person paper check deposit. Mobile check deposit just replaces the physical exchange of a paper check with a secure digital image, but verification, clearing, and settlement must still occur before funds are released. Because of this, mobile check deposit functions as a faster way to initiate the process—not a way to bypass it.

How Mobile Check Deposits are Processed

Once you know what a mobile check deposit is, the key is knowing what actually happens after you tap “submit.” The process that follows determines whether funds are available quickly or require additional review. When a check is submitted through a mobile app, it enters a multi-stage workflow designed to validate the deposit and manage risk for both the bank and the account holder.

- The process begins with endorsement. The back of the check must be signed by the account holder or payee, and banks may require you to check a box or add additional language such as “For mobile deposit only.” This confirms that the account holder approves the transfer of funds and authorizes the bank to process the check, while ensuring it is being deposited through a single channel and preventing duplicate submissions.

- Automated validations take place. Behind the scenes, systems review the deposit for several factors, including:

- Image clarity and completeness

- Accuracy of the entered amount

- Duplicate deposit detection

- Early fraud indicators

- The deposit is reviewed, accepted or rejected. Following this review, the deposit is either accepted automatically or routed for manual verification. High-dollar deposits, deposits into newer accounts with limited transaction history, or checks from unfamiliar sources may require additional review before moving forward.

- Clearing and settlement begin. Once accepted, the bank initiates the settlement process with the issuing bank, where the issuing bank verifies the check and approves the payment.

- Funds are released. After the check has been verified by the issuing bank, the funds are released and made available in your account. Timing may vary depending on the bank, the deposit amount, and your account or transaction history, so some deposits may be available immediately while others are held in accordance with the bank’s funds availability policy.

Pro Tip: A deposit can appear in your account before funds are available. “Posted” means the deposit has been recorded. “Available” means the funds can be withdrawn, transferred, or used for payments.

Mobile Check Deposit Timelines

Timing is often the biggest source of uncertainty when it comes to mobile check deposits. Even though depositing a check—especially via mobile—can feel immediate, the experience varies from bank to bank. There is no single timeline that applies to every mobile deposit. Several factors can influence when deposited funds are available:

- Deposit cutoff times: Deposits made after a bank’s daily cutoff may not begin processing until the next business day.

- Weekends and bank-observed holidays: Banks do not process deposits on non-business days.

- The amount of the check: Larger deposits may trigger additional verification to manage risk and ensure funds are available.

- The type of check being deposited: Personal, business, or government checks can have different processing requirements and clearing times.

- Account and transaction history: New accounts, unusual deposit patterns, or limited activity may require extra review before funds are released.

- Fraud or compliance reviews: Banks perform automated and manual checks to detect potential fraud, prevent duplicate deposits, and comply with regulatory requirements.

Each institution has its own approach to verification, fraud detection, and risk management, which can also affect how quickly funds are made available. Because of this, banks may place holds on certain deposits to protect both the institution and the account holder, ensuring that funds are only released once the check has successfully cleared.